Quartz has an infographic showing the family tress of the six largest beer companies that sell 50% of the world's beer. Consolidation has been huge factor in the beer as an investment story. As anecdotal evidence of the industry's progress, AB Inbev was running ads against itself during the last World Cup.

One could spin a negative story that the industry has been growing by acquisition rather than organic growth and that tastes in major markets have been steadily shifting to wine and spirits.

The positive story is that the industry has recognized changing tastes and that consolidation is a sign of market discipline to keep margins high. Size also creates strong moats around the firms. It would be very difficult for any new entrant to take on the large incumbents in terms of: (1) brewing large volumes of beer of consistent quality; (2) mass marketing; (3) distribution to stores, bars, restaurants, stadiums, festivals, etc; and (4) entering emerging markets where beer can still be a growth story (due to some combination of rising incomes, weak local competitors, and beer as a relatively novel category).

In regards to craft beer: Often delicious. But the trend is not new, and for every successful independent, there are a host of competitors hoping to be bought out by a large multinational.

Disclosures

I hold a material part of my personal portfolio in beer stocks. This is primarily through Ambev, SABMiller, MolsonCoors.

Monday, October 13, 2014

Friday, October 10, 2014

Wednesday, October 8, 2014

Where's the gold?

Ron Paul writes about a Swiss referendum on repatriating their national gold reserves. Some conspiracy theorists will have you believe that this is a major problem because the gold no longer exists. It has been lent out so many times that physical delivery may be very difficult or even impossible without causing havoc with gold prices.

This is not entirely crazy. Like inventories of securities, inventories of gold are traded (or lent). And like securities, sometimes there's going to be a squeeze.

In light of this, and leaving aside the extreme basis that some may hold for the trade, gold as an investment raises practical questions. The costs of acquiring, transporting, storing, and insuring physical gold seem far out of reach for any normal person. But when you buy an ETF, how can you be sure that there's anything in the vault backing it? What other forms of gold can an ordinary investor use?

This is not entirely crazy. Like inventories of securities, inventories of gold are traded (or lent). And like securities, sometimes there's going to be a squeeze.

In light of this, and leaving aside the extreme basis that some may hold for the trade, gold as an investment raises practical questions. The costs of acquiring, transporting, storing, and insuring physical gold seem far out of reach for any normal person. But when you buy an ETF, how can you be sure that there's anything in the vault backing it? What other forms of gold can an ordinary investor use?

Monday, October 6, 2014

Canadian international merchandise trade (balance of payments) - August 2014

Balance of payments swung from a surplus of $2.2B (adj) in July 2014 to a deficit of $0.6B in August 2014. At the product level, Canada exported $0.6B less energy products and imported $0.7B more energy products. Yup.

Friday, October 3, 2014

Share buybacks

There has been much hand wringing and consternation over share buybacks. There's also been WTF BBBuYbacks.

As an investor I can't help but feel good about getting cash back through share buybacks.

However, I do appreciate concerns about having sufficient cash on hand to invest in the business, to pursue opportunistic transactions, and to get through a rainy day. The market is happy to take the money at any time, but is not likely to eagerly reinvest when the company needs the cash. We tried this model in Canada, with income trusts (pay out all your cash, then go back to the market for more money), but the government shut down the trade before it ever went through a real test of faith.

There needs to be confidence that management is going to make good use-of-cash decisions over time--or else why invest in the company at all? So the discussion should pivot from buybacks as the devil, to the proper incentive structure for managements. It's easy to see how management could use buybacks to maximize personal compensation: juice up EPS based bonuses, raise the value of stock options, and make the company a less attractive takeover target (where management would be fired). It is less clear how to fix the situation.

See Aswath Damodaran for an in-depth look at buybacks.

As an investor I can't help but feel good about getting cash back through share buybacks.

However, I do appreciate concerns about having sufficient cash on hand to invest in the business, to pursue opportunistic transactions, and to get through a rainy day. The market is happy to take the money at any time, but is not likely to eagerly reinvest when the company needs the cash. We tried this model in Canada, with income trusts (pay out all your cash, then go back to the market for more money), but the government shut down the trade before it ever went through a real test of faith.

There needs to be confidence that management is going to make good use-of-cash decisions over time--or else why invest in the company at all? So the discussion should pivot from buybacks as the devil, to the proper incentive structure for managements. It's easy to see how management could use buybacks to maximize personal compensation: juice up EPS based bonuses, raise the value of stock options, and make the company a less attractive takeover target (where management would be fired). It is less clear how to fix the situation.

See Aswath Damodaran for an in-depth look at buybacks.

Wednesday, October 1, 2014

Inequality in the 21st century

It is hard to deny that Thomas Piketty's book, Capital in the Twenty-First Century, has lent unprecedented attention to the issue of inequality, both of income and of wealth. It's especially interesting that it has even captured the imagination of the U.S. media and politicians (don't forget the Fed) in a country where no one is poor...they just haven't made it yet!

Technology and productivity are part of the story and I think most reasonable people would say those are both good things. But there's also the issue of fairness. Are there mechanisms to curb outrageous concentrations of dynastic wealth; are there conditions for equal opportunity in the form of (realistic, not hypothetical, not mythological) access to education, healthcare, clean water, nutritious food, clothing, and shelter; are there incentives to innovate, advance our understanding of the universe and improve our (read: humans') standard of living?

This last point is not trivial, so I will digress.

It has been suggested that U.S. economic growth is over due to lack of technological innovation. Try to imagine life without likes or tweets or lolcats or the latest killer app in the iTunes store. Now try to imagine life without indoor plumbing. Where's the real innovation?

The U.S. semi-conductor industry can trace their roots, through predecessor companies, founders, and employees, to public funding, for math, science, and engineering, and big government contracts from NASA. And of course, this was before start-up companies had to contend withcertain death from a broken patent system. What is the contemporary example of hardcore public support for the so-called STEM fields?

My mental model of this stuff is that it takes 5 years to put together a salable new product or process. It probably rests on the work of 10 years of engineering research in novel and useful areas. But that engineering rests on the results of 100 years of basic research in math and science. That's 115 years of R&D.

Thoughts as an investor:

Technology and productivity are part of the story and I think most reasonable people would say those are both good things. But there's also the issue of fairness. Are there mechanisms to curb outrageous concentrations of dynastic wealth; are there conditions for equal opportunity in the form of (realistic, not hypothetical, not mythological) access to education, healthcare, clean water, nutritious food, clothing, and shelter; are there incentives to innovate, advance our understanding of the universe and improve our (read: humans') standard of living?

This last point is not trivial, so I will digress.

It has been suggested that U.S. economic growth is over due to lack of technological innovation. Try to imagine life without likes or tweets or lolcats or the latest killer app in the iTunes store. Now try to imagine life without indoor plumbing. Where's the real innovation?

The U.S. semi-conductor industry can trace their roots, through predecessor companies, founders, and employees, to public funding, for math, science, and engineering, and big government contracts from NASA. And of course, this was before start-up companies had to contend with

My mental model of this stuff is that it takes 5 years to put together a salable new product or process. It probably rests on the work of 10 years of engineering research in novel and useful areas. But that engineering rests on the results of 100 years of basic research in math and science. That's 115 years of R&D.

Thoughts as an investor:

- Long term investing is relative. In 115 years we'll all be dead. In the absence of strong public sponsorship, investors will tend towards the path of least resistance and buy the nonsense (either of the Bay Area or Wall St variety) even if the present value of truly innovative R&D is exponentially higher and more beneficial for all of humanity.

- There is a riskiness in a society that concentrates wealth and power to extremes. I worry about the U.S. where it is legal to buy the government and where there is an origin story based on violence in the face of unjust rule. Remember, "No taxation without representation!"

- The plebs are multitude and the elites are, well, elite. I have to believe in the benefits of a trickle up effect more than a trickle down effect. It is a matter of surplus. Billionaires are hoarding cash while people in U.S. cities are living in food deserts and without clean running water. Give someone at the bottom $1,000 and it goes straight into the (local) economy. Give a billionaire $1,000 tax break... and who knows.

Monday, September 29, 2014

Bought Lululemon (LULU)

I bought a small amount of Lululemon (LULU) within recent weeks at an average price around $40. This is intended to be a short to medium term trade.

Support for the trade:

Support for the trade:

- Stock is down 50% from recent historical highs

- The scuffle with founder Chip Wilson has calmed after the deal with Advent International

- Advent knows this business very well and their involvement is a positive signal

- No debt, strong cash position

- A profitable business with loyal customer base

- I don't believe the core customer will migrate to cheaper alternatives--do you really want to show up at mommy&me yoga wearing the discount brand?

Potential catalysts:

- M&A, inversion transaction?

- Share buybacks

- Continue to 'beat' quarterly analyst expectations

- Positive signals from international expansion

Risks:

- Less appealing acquisition target from use of cash for buybacks and the U.S. crackdown on the tax inversion trade

- Continued downward trend on comparable store sales

- Poor execution in the direct to consumer channel

- Poor results from international foray

Friday, September 26, 2014

Good news, bad news in U.S. jobs data

I looked at some Canadian labour force charts quite a while ago (here and here).

It is a pain to manually create charts in Excel so I thought I'd look at some U.S. charts using the amazingly awesome charting tool, FRED, at the St Louis Fed.

First up, the good news. The underemployment rate (as measured by the "U-6") has come down markedly from its highs. There seems to be some debate among economists (at least the kind on TV and radio) as to whether or not unemployment rates will ever go back to 'normal' levels. In other words, is there a new NAIRU. But for now, the trend seems to be for lower rates of unemployment and underemployment. Supporting this idea, hours worked has recovered nicely from the lows. Clearly, more people working and firms requiring more labour hours is a good thing.

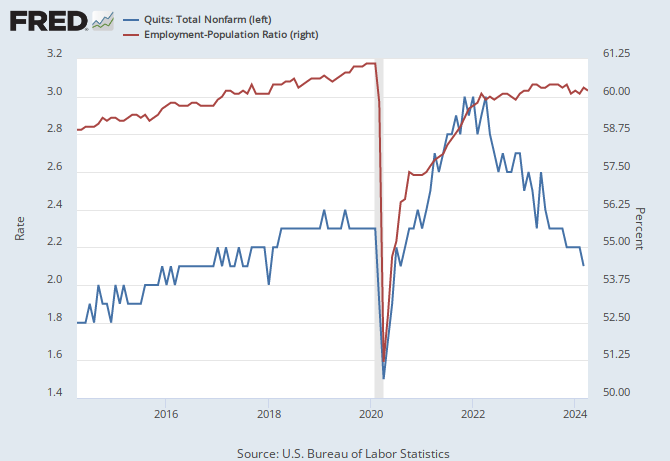

Now the less good news. While the quits rate has also improved from the lows, it's still below a 'normal' 2%-ish rate (although we'll have to wait and see if it continues to trend higher or flattens out here). This may be hinting at continued friction or lack of choices for workers trying to move jobs, and improve their lot in life. The big bad news is the size of the working population. Post-Great Recession, a great percentage of the population seem to have stopped working--or at least stopped being counted.

It is a pain to manually create charts in Excel so I thought I'd look at some U.S. charts using the amazingly awesome charting tool, FRED, at the St Louis Fed.

First up, the good news. The underemployment rate (as measured by the "U-6") has come down markedly from its highs. There seems to be some debate among economists (at least the kind on TV and radio) as to whether or not unemployment rates will ever go back to 'normal' levels. In other words, is there a new NAIRU. But for now, the trend seems to be for lower rates of unemployment and underemployment. Supporting this idea, hours worked has recovered nicely from the lows. Clearly, more people working and firms requiring more labour hours is a good thing.

Now the less good news. While the quits rate has also improved from the lows, it's still below a 'normal' 2%-ish rate (although we'll have to wait and see if it continues to trend higher or flattens out here). This may be hinting at continued friction or lack of choices for workers trying to move jobs, and improve their lot in life. The big bad news is the size of the working population. Post-Great Recession, a great percentage of the population seem to have stopped working--or at least stopped being counted.

Wednesday, September 24, 2014

Sold stocks

In line with my thoughts in a previous gold post, I've finished selling substantially all of my general stock market exposure. For me, this was XIU, ACWI, VIG, and EEM. This took place over several months and a good deal of it was reinvested into gold ETFs. The remainder is in cash. So far, this has been a terrible trade as stocks have continued to trend higher and gold has gone the other way.

I continue to hold most of my portfolio in single name stocks.

I continue to hold most of my portfolio in single name stocks.

Monday, September 22, 2014

Gold, and the end of the world as we know it

From time to time I come across websites describing the imminent financial end of days, and how only those with gold (and presumably guns) will survive. The basic idea goes like this: weak economies and decaying civilizations are being propped up by governments and central banks through manipulation of financial markets, unduly benefiting the elite in the process, and the price of gold must be artificially suppressed to mask any signal of the true (i.e. low) value of fiat currency and financial assets. The day of reckoning is coming.

While this all seems a bit extreme, I do wonder what harm all the extraordinary monetary measures, deployed over the last several years, are causing. Presumably there is a bubble forming somewhere. Add to that concern, the disproportionately lackluster response from the real economy reveals deep problems that will not be solved any time soon.

While this all seems a bit extreme, I do wonder what harm all the extraordinary monetary measures, deployed over the last several years, are causing. Presumably there is a bubble forming somewhere. Add to that concern, the disproportionately lackluster response from the real economy reveals deep problems that will not be solved any time soon.

Subscribe to:

Posts (Atom)